The German chancellor - Angela Merkel - described the European debt crisis as "maybe Europe's most difficult hours since world war two". Merkel doesn't seem the kind of politician that over-cooks her messages. If this is indeed a moment of extreme crisis, then it is time to examine worst-case scenarios.

The European single currency is close to collapse. Already French and German civil servants are putting together a strategy whereby some of the Eurozone members re-introduce national currencies. When chaos is raging, technocratic solutions are beguiling. They provide a reassuring sense of order and calm.

If only the world could be crafted like the outlines of PowerPoint presentations and strategy papers. Unfortunately, once the Eurozone begin to disintegrate, those carefully drafted plans will be quickly consigned to the circular filing cabinets below minister's desks. There will be no orderly departures from the single currency. The eurozone collapse will be ugly and brutal.

It will start with Greece, who will set off a chain reaction of Eurozone departures. Like falling dominos, one Eurozone country after another will be forced to reintroduce their national currency. There will be a race to the bottom as each exiting country devalues to steal jobs from their neighbours. The likeliest outcome will be 17 European currencies where there is currently only one.

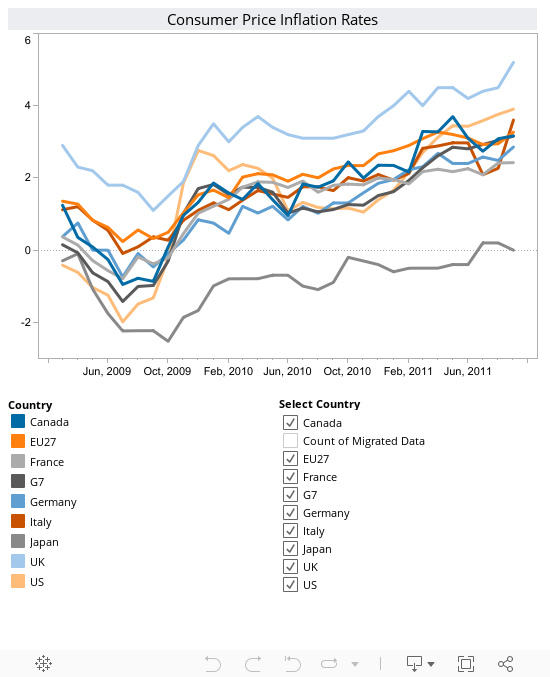

Eurozone disintegration will be immediately followed by a massive surge in inflation. Countries like Greece can reasonably expect the value of the new currencies to drop by half, as exchange rates realign with underlying fundamentals. If Europe is lucky, it will avoid hyperinflation. If not, we can expect the value all European financial assets to be wiped out within months. Imagine a continent of ageing hippies without savings, and you will be about 10 percent of the way towards understanding what the post-EMU Europe will look like.

Inevitably, output will collapse, the financial system will disintegrate, and unemployment will go through the proverbial roof. The great depression will look like a gentle blip compared to the implosion of the Europe.

These are just the short run consequences of Eurozone disintegration.It is anyone's guess as to the political consequences of the total destruction of the European economy. Nevertheless, the very idea of the European Union will suffer catastrophic shock. Member countries will naturally begin a long and vicious period of mutual recrimination. Germany will blame Southern Europe; France will blame Germany, while many in Britain will say "I told you so". Efforts to create an "ever closer union" will be abandoned, probably forever. In the short run, the infrastructure of union is likely to remain, but few will take it seriously. The European Union would become a wretched institutional mess hanging over Europe.

Many will welcome the demise of the European Union. Certainly, European integration has been running at a pace far faster than the vast majority of ordinary Europeans were willing to accept. Animosity towards the EU had been growing across Europe long before the current crisis. European integration had become a cynical exercise where politicians routinely ignored the wishes of their electorates.

However, the European enterprise was created to conceal the deep and unpleasant truth. There was a time when Europe dominated the world, but for at least 50 years or possibly longer, Europe has been in decline. This retreat has taken many forms; political, demographic, military, economic, and cultural.

The creation of a quasi-European state sustained the pretense that Europe still mattered. European politicians in rapidly diminishing states like France, Italy and the UK could argue that Europe still mattered. Rather like the Greek public debt numbers, the claim was based on false accounting. Adding together 27 decrepit and ossified countries does not create a dynamic superstate. Once the Eurozone goes, that conceit will be finally exposed.